Why Algo-Stable Bonds Don’t Work

(Disclaimer: Author is a Strategist with MITH Cash)

TL;DR version: Algo-stable bonds don’t work because bonds involve “supply contraction” — a relatively “weak force” in pushing the algo-stable’s price up. It is weak because bond-buying usually entails no purchase of MIC (Mith Cash’s algo-stablecoin) and only deters selling in a fraction of cases. In contrast, buying of MIC is a “strong force” for moving the algo-stablecoin up in price because it has Full Impact instead of Fractional Impact (that bond buying does). Each MIC bought will have a positive impact on the price every time ; it is not guesswork. Therefore, I suggest we de-prioritize bonds and recommend ways to incentivize Sub $1 buying through rewards (leveraging the Synthetix fees/rebates model) as well as propose ways to incentivize group buying as well.

The algorithmic coins Basis Cash and MITH Cash are all the rage today. Paul Veradittakit, a partner at Pantera Capital, just recently wrote a very clear summary of what algo-stables are and how they work as a helpful backgrounder.

Additionally, Yearn and Curve announced metapools, where anyone can create their own trading pool against Curve’s Y-Pool token or Curve’s sBTC-Pool token. Their first implementation was using Basis’s BAC and MITH’s MIC (along with algo-stables FRAX, DSD, and

ESD). To see it, check out: https://crv.finance/ .

Algo-stables are attracting this kind of attention for two reasons:

- The insanely high yields we’ve seen on farming them where MITH and BAC topped the yield-farming lists in APY% return since inception- posting returns north of 1,000% a year

- They represent the true alternative to fiat currencies. Unlike fiat-backed currencies like USDC or crypto-backed currencies like DAI, algo-stables are not bound by the amount of collateral deposited backing them.

Just like the dollar was able to scale in a growing American economy and as a global reserve currency as it untethered itself from the gold standard in 1933 (and the remnants of it in 1973), so too can crypto stablecoins scale effectively if it can remain stable without collateral backing. The operative word in the last sentence is “IF”.

Background

Prior algo-stables Empty Set Dollar (ESD) and Dynamic Set Dollar (DSD)- which began in late 2020- have lagged below the peg in the $0.60 and $0.70 range. After high-flying, both Mith Cash (MIC) and Basis Cash (BAC) too find themselves under-peg hovering between $0.55 and $0.85. You can still profit from farming the share tokens for these coins by providing liquidity to their pairs on Uniswap and Sushiswap — but for how long? Retaining the peg is essential for long-term success of an algo-stable.

The algo-stable field has yet to hold peg. Knowing this, each new algo-stable risks mindlessly repeating the failures of the past coins by borrowing the Bond-Coupon/Share-Bonding system with little modification like a crypto equivalent of the movie Groundhog’s Day where Bill Murray is stuck in a time loop creating failed stablecoins each day (ok the analogy needs some work!).

If we want these new algo-stables to hold peg, we need to ReThink whole sections of the algo-monetary system we inherit from the last project not merely repeat the mechanisms of past algo-stables with merely modest improvements. We must be ready, after analysis, to rip & replace sections of the monetary system — in order to get the qualitative change we need to be stable at peg.

Algo-Stables have a Natural Supply/Demand Imbalance which leads to a Persistent Under-Peg

The biggest issue facing algo-stables is under-peg, or having a price underneath the target price of $1. All major algo-stables are currently under peg. This is because of an imbalance in Supply and Demand. On the supply side, the supply of an algo-stable like MIC is 35 million. The demand? There is little unique you can do with MIC that you cannot otherwise do with a collateral-backed stable like DAI or USDC. The primary demand is in using MIC to farm the share token (MIS). This is not a criticism of MITH; every algo-stable has roughly the same Supply/Demand imbalance.

Compare this imbalance to the relative balance in supply and demand of the US dollar. The demand is that you can really only procure services and products in the United States using dollars. Try going into a Home Depot sometime and try paying with your homemade brass quatloons that you forged in your own basement, and see how that goes (practice rolling as you fall ahead of time for when Home Depot security tosses you out the door). The demand for the US dollar is astronomical; and that doesn’t even consider its use as a global reserve currency across other nations.

Because algo-stables and nation-state sovereign currencies function in such different environments, borrowing techniques that central banks use to stabilize may not work with the same efficacy in the algo-stable micro-environment. Each technique must be evaluated on its own real-world merits in the unique algo-stable environment considering different supply/demand dynamics as opposed to the concept’s academic legitimacy.

Eventually, projects will cultivate demand for their coins, but until then the question is how do you stabilize until that demand is generated? I address some of this in my last piece on guardrails- discussing centralized stabilization and selective restrictions on sub $1 trading. Today, I’ll discussing bonds. I’m not a fan and I’ll tell why.

Why Algo-stable Bonds don’t get the Job Done

The algo-stable mechanism of bonds, as defined by Basis, from which many algo-stables are now based, does not function like you and I are used to thinking about bonds. It shares the name of “bonds” in common and it contracts the money supply. The rest is quite a bit different.

Let’s take an example using MIC stablecoin. For this example, I will ignore certain complexities such as Time Weight Average Price (TWAP), epochs, and some detailed mechanisms for simplicity’s sake.

Let’s say MIC drops from $1 to $0.80. At that point, you can buy a MIB (bond token) for the spot price squared so $0.80 * $0.80 = $0.64. A decent discount of: 20%! When you buy the bond, your MIC that you bought it with is held by the project smart contract (taken out of supply). When MIC goes back up to $1, you can redeem the bond. Redeeming means the project gives you $1 of MIC and it burns the MIC you deposited initially to buy the BAB. The bond holder has made a terrific 56% profit (buying at $0.64 and selling at $1), granted with a degree of risk in that you had to bet on MIC returning to $1.

But what is the global impact to MIC? In the short-term, bonds contract the MIC supply. But long-run the supply remains the same because bonds result in the holder being given MIC when redeeming which cancels out the MIC that is burned upon redemption. If we are to believe that the contraction is what led to MIC regaining its peg, maybe we could say bonds have value. My observations are that’s not happened. In fact, the opposite seems to be happening where whales game the system to de-peg the coin, profit from bonds, and repeat.

The Declining “Cost Basis” Problem of Algo-Stable Bonds

Let’s continue the example. We spoke earlier about Supply-Demand Imbalance. A related concept is Buy-Pressure and Sell-Pressure of the algo-stable. To explain this concept in this context, let me talk about the buy-pressure for a dollar. You need US dollars to buy really anything, so if one day you saw you had no dollars (maybe you misplaced them all!), you would take out whatever you had in your apartment and sell them on the street, at a discount, for those dollars. That’s how badly you needed them. In other words, the demand for dollars, the utility of them is so high (they are necessary) that you would readily lose money on assets to acquire them. The buy-pressure is high. That is a stabilizing force for a currency.

In contrast, the sell-pressure is high for algo-stables like MIC; this means people readily sell them (typically into mainstream stable coins). Why? The background here is important. To get a US dollar, you have to work for it. You have to get a job usually and provide some valuable labor. You value the dollar because you put real work into it and you won’t accept less value than what you put in.

In contrast, for an algo-stable, typically you got it at first for “free” from the genesis seed pool event, then later got it as “profit” from farming the token, and then later received more of it through seignorages (new MIC given to shareholders over time based on certain criteria). Holders are eager to sell to take profit (or minimize losses). Further, there is risk of holding (volatility) and at present, not many use-cases to apply it too (although that will change).

Bonds add to this problem. Why? Because from the earlier Bonds example, we can see that a MIC holder can pay $0.64 worth of MIC to get a Bond and then later receive $1 worth of MIC. Maybe he bought his first MIC at $1 (cost basis) but now his cost basis is reduced to $0.64. So now you have a large supply of MIC out there with an even lower cost basis, which furthers the sell-pressure because holders will gladly sell at $0.80 cents or even $0.70 to net a profit. The bond system constantly lowers the cost basis on MIC holders — worsening the Sell Pressure/Buy Pressure balance. Over time, with more bond issuances, a kind of liability is incurred where the algo-stable has distributed currency at discount and the ensuing selling will likely ensure it goes back to underpeg.

One reason for the “cost basis” problem of algo-stable bonds is the steepness of the bond discount on MIC, which could be fixed through improving the bond mechanism. But as I’ll explore next, the “cost basis” problem is not even the most problematic part of algo-stable bonds.

Why we Must Think Beyond Bonds

It is difficult in an economic system to disambiguate the effects of specific factors (like bonds)in stabilizing the algo-stable to its $1 peg because so many factors are at play (ie: whales buying in/cashing out, new events that cause demand for MIC or for a rival, causing MIC to be traded for BAC, etc.). The algo-stable landscape changes quickly, complicating this further. For MIC, Harvest and then Pickle offered amped-up yield farming for the MIC/USDT pair, with yields of over 1000% APY. Suddenly huge numbers bought MIC for that reason and we were at peg or above. Then a few days later, a new project Basis Gold launched and featured a BAC seed pool but none for MIC. MIC holders saw an opportunity to profit with BAC so they sold MIC en masse to acquire BAC; this had an underpeg effect on the MIC price. Due to these massive shifts from individual events, it is hard to isolate the effect bonds had during these times in achieving the peg.

However, my sense from observing the data and evaluating transactions as well as the price action of MIC is that contracting the supply does not seem to make much of a difference. The effects are not felt because: i) too little of the supply ends up being contracted (1/35th for example) and its effect are overwhelmed by other buy/sell factors for the remaining supply, ii) that supply contraction does not last long and then its redemption results in the holder receving the algo-stable again and quickly selling the proceeds, putting the coin back under peg.

I believe we must resist the temptation to merely tinker with the bond mechanism, as designed, but also consider and prioritize other approaches. Contraction may work on a macro nation-state scale but given the supply/demand imbalance of algo-stables we need stronger forces.

Let’s borrow verbiage from science. Quantum physics has what it calls “strong forces” and “weak forces”; with the strongest force being the nuclear force that holds particles together. In algo-stables, we’ve used the weak force of bonds for a while, and it has not solved the underpeg issue. Empty Set Dollar, Dynamic Set Dollar, and many others have found that out the hard way. Even if you play with durations, yields, terms of payout, buying mechanism, many of the problems still persist.

Why are algo-stable bonds a “Weak Force”?

When you buy a MIB bond, you are betting MIC will go up in price. What are you doing is locking your MIC to later unlock if MIC reaches $1 — and receive an amplified profit it does. This accomplishes supply contraction. This prevents the holder of MIC from selling MIC. But what are the odds the holder would sell? His pre-bond-purchase options were:

- Hold: and wait for MIC to go up

- Farm: use MIC to farm for MIS (whether directly or through Harvest/Pickle)

- Sell: Rage-quit out of the algo-stable and get out, even at a sub $1 price

As you can see, Selling is only one of three options.

Let’s take a scenario where someone used their MIC to buy MIB. That MIC holder may have been farming MIS with it— as it can be profitable, granted with risk. Or maybe they were holding on MIC not wanting to risk impermanent loss on farming, waiting for it to edge up and gain a profit. Only a fraction were considering selling before considering the bond opportunity. So bonds only have a Fractional Impact on the Buy-Sell ledger for MIC in favor of pushing the price up. In that the existence of bonds only prevented a fraction of MIC holders to hold who otherwise were intent on selling.

The absolute worst part about algo-stable bonds is that it discourages buying of MIC. Buying is a “strong force” — it necessarily impacts the Buy-Sell ledger on the MIC currency 100% of the time in pushing the price up. This can be considered Full Impact. Buyers of MIB bonds typically already own MIC. So using MIC to buy a bond does not have any strong force impacts on the price of MIC because there is no new buying of MIC (as mentioned though, it does prevent some fraction of selling). In a world without bonds, if a MIC holder saw the low MIC price, they might ordinarily buy MIC at the low price to add to their position (that would have a strong impact on MIC price). But with bonds, they will not do this; they will opt for the higher yield and buy MIB instead of MIC (replacing a strong force with a weaker force on MIC’s price).

Put simply: Full impact (Buying MIC) > Fractional impact (Buying Bonds).

The “Strong Force” to combat the Underpeg: Incentivized Buying and Coordinated buying

So how we do replace the weak force (of Bonds) with a strong force (of Buying MIC)? By incentivizing buying MIC when it’s under $1. Buying MIC is a stronger force to solve the under-peg than buying a bond because it has Full Impact in terms of impacting the MIC price upwards instead of Fractional Impact of bond-driven supply contraction.

In this proposal, those who would buy MIC when the price is below-peg receive a reward token during the purchase. This can be included at the time of purchase and facilitated by the token smart contract. This reward could be a newly introduced project token for MITH, or it may be payable in MIB or MIS. (“Buy” rewards implementation would have to be coupled with a “Sell” tax in order to prevent rapid buy-sell behavior by investors to accumulate rewards but without truly supporting the MIC price.)

One model for algo-stables in building this feature is Synthetix’s Rebates/Fees. When I mention this, I do NOT mean that we will implement Rebates/Fees the same way Synthetix did; they use this method to prevent gaps in prices between their synthetic assets (ie:sETH) and the underlying asset (ETH). Our goal is different- to penalize Sub $1 sales, and reward sub $1 purchases. Where we can learn something is from how Synthetix cleverly used their token contracts to impose these fees and offer rebates to people doing transactions with their synths anywhere (not just on the Synthetix Exchange), just as we can impose taxes on Sub $1 TX and offer rewards for sub $1 buys for MIC anywhere (Sushi, Curve, etc.)

Without going into detail on Synthetix’s specific implementation (more can be read at the link above), their fees/rebates model suggests certain things are possible for Mith Cash:

- It is possible to use the token contract to restrict certain transactions (see my prior piece for restrictions on certain Sub $1 tx). Synthetix stops certain transactions based on a “waiting period” or if the user has not paid their fees owed; they’re not able to send further transactions.

- We can issue taxes and offer rewards based on the nature of transaction. Synthetix notifies users on the partner page (ie: Curve), and has a link to “settle” the charges.

- We can direct users who are either taxed or rewarded to a separate page where they can receive or pay, and on that page we can explain things clearly (so we won’t have confused MIC users). Just as Synthetix does with their users on their “settle” page.

- We can issue the tax or reward after the TX while permitting it with the penalty being that they cannot do another TX with MIC until they resolve the tax involved. Synthetix does not thwart the original transaction. They add the fee/reward after and enforce it by locking their synths until you settle.

- We must collaborate with 3rd parties where MIC is traded (Sushiswap, Curve) for them to provide visual cues and text explaining the situation. Synthetix sets a good example in this in how they’ve worked with Curve to walk their users through these fee/rebate situations. (see below for example of this) Otherwise the user will be in a state of confusion.

Alternate Implementation of Sub-$1 Buy Incentives for Individuals

Another way of incentivizing buying other than through the token smart contract is to setup a facility MITH provides on its website that handles the smart contract logic of the Sushiswap trade and furnishes the reward (if this is technically feasible). The advantage of this approach is:

- More control over the transaction and user experience- more clearly explaining the whole process, which is harder to do through 3rd party sites.

- Offer a wider variety of rewards that are clearly spelled out

- Lock the newly purchased MIC (for some period of time to maximize durable benefit of the buy order); or give the user the option for an extended lock for additional rewards

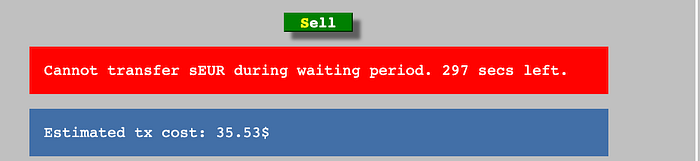

Some of this may be possible through a token contract as well, but requires closer coordination with 3rd party sites. An example of this coordination would be Synthetix’s coordination with Curve, so that the end-user is clearly notified about the Fee/Rebate impact on their “synthetics” transactions. Here is it at work:

At another time, I was asked on Curve’s site to click to ‘settle’ a transaction with SEUR (a synth) — there was a link to click on where presumably more information would be available on the rebate I was owed and allowing me to collect it (I was in a hurry so I didn’t bother).

In this case, Curve clearly communicates the logic of the impacts of SEUR’s token contract to the end-user and then lets the user click to a page to deal with rebates/fees.

Sub $1 Buy Incentives — other than Individual Incentives

- Batch model: Incentivized buying could also be accomplished in a batch model where investors contribute money to a buyback fund. That fund then buys back the MITH currency and returns it to investors with rewards such as project tokens, MIB or MIS. The amount of rewards may be proportional to how far MIC is from its $1 peg. A locking period may be essential to ensure the effect of the buyback persists. The advantage of this approach is more flexibility in the project providing rewards as it avoids the complexity of issuing rewards through the token contract.

- Outsourced model: Solutions like Stabilize incentivize individuals to shore-up the price of stablecoins by offering buy-side incentives using their own token as a reward. Stabilize currently works with ESD, DSD and BAC. (note: I have not yet fully studied the details of Stabilize).

- Project-led model: Institute a project-led stabilization fund. I touched on this in my last piece. The best way to fund this stabilization fund is through a newly created project token for Mith. It then converts these to a mainstream stablecoin (like USDT) and makes regular purchases of the algo-stable. Independent economic actors have limits in their support of MIC’s price; for example, when the price of MIC is very low (ie: $0.50), that may be an excellent time to buy. But the independent actor is plagued with fear and also lacks things like advanced MIC demand models that the project may have that informs their MIC buying. A fund would complement the actions of independent actors in supporting the MIC price.

In Conclusion

It’s not surprising to see many algo-stables mired at $0.50 or so. Bonds cannot lift them out of that predicament as they employ a fractional-impact “weak force” on the algo-stable price. Long-term, building demand for the algo-stable will ultimately increase and stabilize it’s price. But for the forseeable future, for the reasons mentioned, improving incentives by rewarding sub $1 purchases of the algo-stable may be the best way to stabilize the price when it is under-peg